SMM News on December 5:

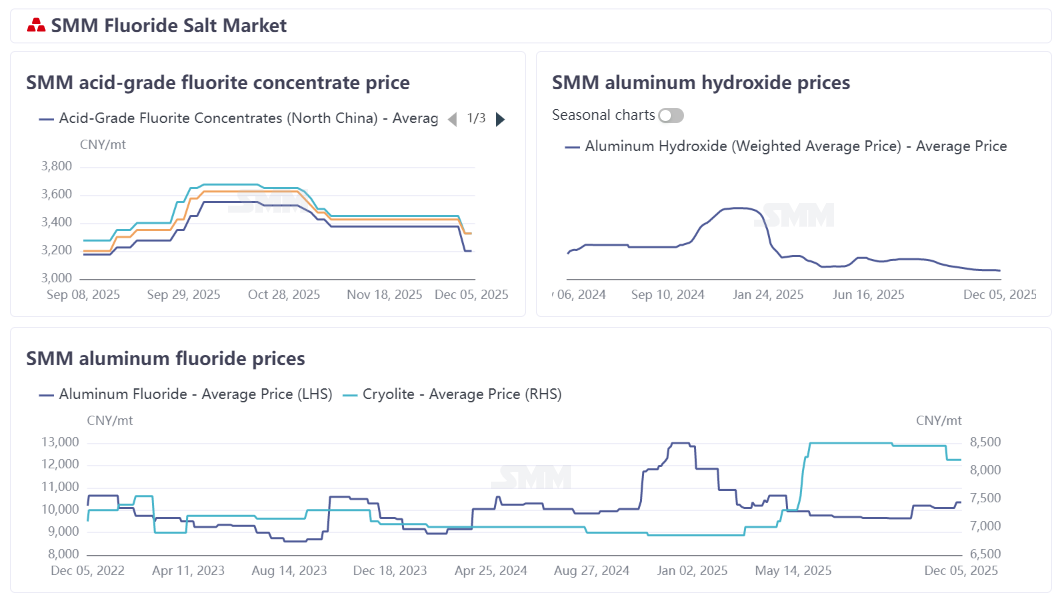

In November, aluminum fluoride prices declined due to earlier weakening in fluorite and aluminum hydroxide prices. During the month, SMM aluminum fluoride prices closed at 9,940–10,250 yuan/mt. The cryolite market saw a slight price drop as demand turned mediocre, with SMM cryolite quotes at 7,400–9,000 yuan/mt. Entering December, aluminum fluoride prices generally increased, supported by rising sulfuric acid raw material costs. As of now, SMM aluminum fluoride prices closed at 10,200–10,500 yuan/mt, while cryolite prices remained stable.

On the raw material side, fluorite prices fell in November before stabilizing. Supply side, although affected by mine safety and environmental protection rectifications, slow release of new capacity, and the elimination of outdated capacity, the industry’s overall operating rate was not significantly impacted, and spot supply remained stable. Combined with high social inventory and sluggish shipments, prices were directly suppressed. Demand side, performance was weak, with core downstream hydrofluoric acid industry operating rates remaining low. Against a backdrop of corporate losses, purchase willingness was insufficient, making it difficult to effectively support fluorite prices. Entering December, fluorite market fundamentals showed no improvement. Coupled with strong downstream sentiment to drive down prices and low purchase willingness, prices fell further. According to SMM data, as of December 5, the average delivery-to-factory price of SMM 97% fluorite powder reached 3,283 yuan/mt, down 5.3% from November 5. As another key raw material for aluminum fluoride, the aluminum hydroxide market remained weak, but the decline narrowed compared to the previous month. As of December 5, the average ex-factory price of aluminum hydroxide tracked by SMM was 1,749 yuan/mt, down 1.46% from November 5. In addition, the sulfuric acid market continued its upward trend. Driven by tightening supply and strong cost support, sulfuric acid prices climbed steadily during the month. In Shandong, the delivery-to-factory price of sulfuric acid for aluminum fluoride plants had risen to over 1,000 yuan/mt. Entering December, sulfuric acid prices showed no clear weakness and are expected to remain difficult to lower within the month. Overall, although aluminum hydroxide and fluorite prices fell, aluminum fluoride costs increased due to the sharp rise in sulfuric acid prices.

Supply side, in November, aluminum fluoride enterprises faced dual pressures from compressed profit margins and high production costs, leading to persistently low production enthusiasm. Most enterprises incurred losses, with inventory remaining at low levels. Additionally, some enterprises in Henan Province experienced production restrictions due to environmental protection-related controls, resulting in a contraction in overall market supply. Entering December, rising aluminum fluoride prices contributed to a recovery in enterprise profitability, slightly improving production enthusiasm and leading to a modest increase in supply. Overall, the market maintained an adequate level of supply. Demand side, downstream operating aluminum capacity remained largely stable, providing a solid foundation for rigid demand for aluminum fluoride. However, sufficient inventory at some enterprises led to a decline in overall procurement activity, exerting some downward pressure on market prices.

Brief Review: At the beginning of the month, the December tender pricing set by leading downstream aluminum enterprises was officially finalized. The tender prices generally trended upward, settling in the range of 10,200-10,300 yuan/mt. With the clarification of tender prices, aluminum fluoride prices generally increased by 250-300 yuan/mt following this guidance. Cost side, the core raw material for aluminum fluoride, sulphuric acid, continued its strong price trend, providing solid support for aluminum fluoride costs. Meanwhile, the price of another key raw material, fluorite, experienced a pullback, alleviating some production pressure on enterprises and contributing to a slight improvement in industry profitability, which in turn boosted production enthusiasm. Demand side performance remains the main constraint in the current market, with no significant improvement in downstream procurement pace. The overall demand atmosphere remains mediocre, and effective synergistic support between supply and demand has yet to materialize. Subsequent attention should focus closely on dynamic changes in raw material costs and adjustments in the downstream procurement pace.